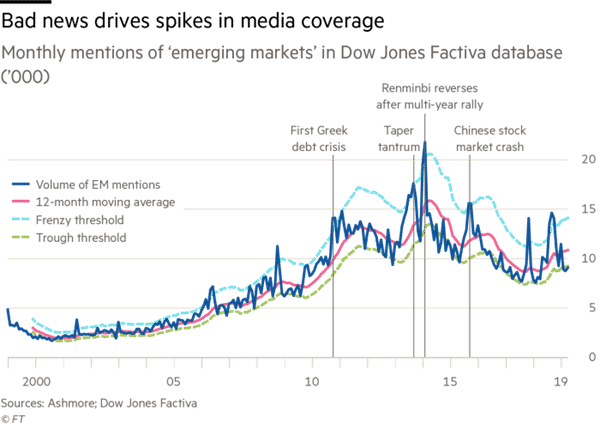

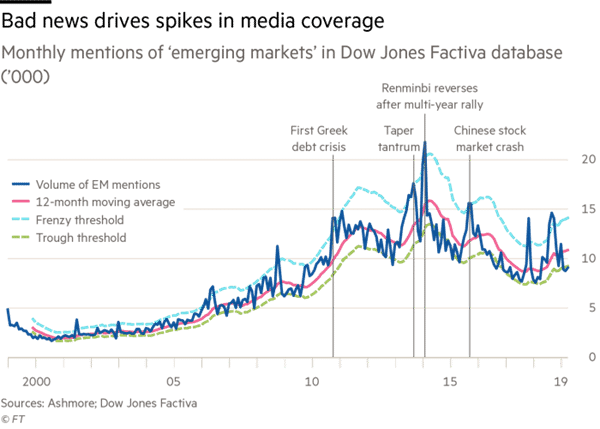

Returns from emerging markets are best when headlines are worst

Ashmore crunches 20 years of news to find that media ‘frenzies’ are good opportunities

Number-crunching by Ashmore suggests the best time to buy EM assets is during media blitzes — all driven by bad news — while the worst is when the EM world is so tranquil it barely garners a column inch. Their analysis suggests an investor who bought only during these periods (and left the money invested) would have received excess returns of more than 10 percentage points a year from EM equities, on top of the underlying profits of 4.1 per cent from a “media-agnostic” strategy of constantly drip-feeding money into the market. EM bonds, too, would have offered significant out-performance.

Hong Kong stocks’ widening discounts leads to increased buying from mainland traders

- Southbound investments via the stock connect schemes in June are headed for the highest level this year

- Gauge compiled by Hang Seng Bank shows that Chinese equities are almost 30 per cent more expensive than their Hong Kong counterparts

Hong Kong stocks now have a potential price catalyst: a widening discount to shares on the Chinese mainland’s exchanges.

STOCK OF THE WEEK

Hollysys Automation Technologies Ltd. manufactures automation and control systems. The Company produces process, industrial, rail and subway, and nuclear power plant automation equipment.

Why I Like Hollysys Automation Technologies Ltd. (NASDAQ:HOLI)

Hollysys Automation Technologies Ltd. (NASDAQ:HOLI) is a company that has been able to sustain great financial health, trading at an attractive share price.

Flawless balance sheet and good value

HOLI’s strong financial health means that all of its upcoming liability payments are able to be met by its current cash and short-term investment holdings. This indicates that HOLI has sufficient cash flows and proper cash management in place, which is a key determinant of the company’s health. HOLI appears to have made good use of debt, producing operating cash levels of 6.02x total debt in the prior year. This is a strong indication that debt is reasonably met with cash generated. HOLI’s share price is trading below its true value according to its price-to-earnings ratio of 8.71x compared to its industry as well as the wider stock market, making it a relatively cheap stock compared to its peers.