Q3 2020

Description: At Milltrust, we have developed proprietary geographical asset allocation models that help drive the country allocation recommendations for our equity investment solutions. The models are based on a scoring mechanism that compares and evaluates the attractiveness of each country using quantitative investment factors that have been shown to convey information about future equity returns. This allows us to tilt the portfolios towards the countries and regions that provide a more favourable environment with the goal of enhancing dollar returns of unhedged global equity portfolios. This is a systematic process.

Strategy: Milltrust Global Emerging Markets Equity Strategy

Investment Universe (core – 10 countries): China, Taiwan, India, South Korea, Thailand, Malaysia, Indonesia, Brazil, Russia and South Africa.

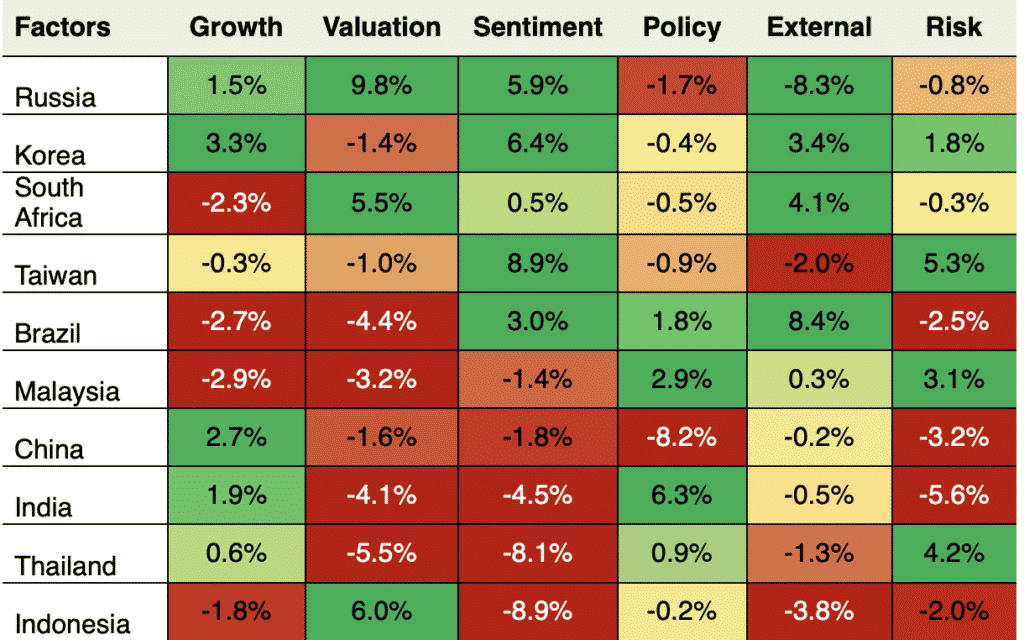

Summary: There has been some movement in the rankings for the upcoming quarter with South Africa moving to an overweight as valuations reach very attractive levels. Other movers include China moving up to neutral as the economy proves to be increasingly resilient, Brazil dropping down slightly from an overweight position due to their expensive valuations and Indonesia becoming an underweight as it falls into the value trap category with poor growth and momentum indicators. We continue to view Russia, South Korea and Taiwan as the best country bets.

Highlights:

- Overweight: Russia, South Korea, South Africa and Taiwan

Russia remains the top ranked country in our model with the double benefit of offering attractive valuations and high dividends; the year-on-year price momentum is also still positive. South Korea is another overweight and has been resilient from a growth perspective with growth forecasts for 2021 improving 70 bps over the last six months; Year-on-year price momentum remains positive, the currency is undervalued and the terms of trade is trending up. Meanwhile, South Africa has seen its growth forecasts increase 140 basis points for 2021 supported by an improving terms-of-trade trend while offering attractive valuations with its current forecasted P/E ratio below both the EM average and its own 10-year average. The rand is also undervalued in real terms. Finally, Taiwan’s attractiveness is boosted by their positive price momentum and favourable risk indicators including a substantial current account surplus relative to GDP.

- Neutral: Brazil, China, Malaysia,

Similar to South Korea, China’s economy is rebounding faster than others with GDP growth forecasts increasing 230 bps for 2021; however, monetary conditions are still relatively tight with loosening action by the authorities slower than other EM countries. Brazil has fallen down the rankings to a more neutral allocation mainly due to expensive valuations; its forecasted 2020 PE ratio is above the overall EM average and its own long-term average. On the other hand, the Brazilian Real continues to be extremely undervalued and monetary policy becomes increasingly accommodating. Finally, Malaysia has been bringing down interest rates in line with the EM average and still has relatively high real interest rates to work with. The risk factors are also favourable for the country which has healthy external balances.

- Underweight: India, Thailand, Indonesia

India’s domestic growth has been more resilient in 2020 but there are concerns over 2021 growth as forecasts drop below the EM average. India’s forecasted 2020 PE ratio is in line with EM average, but price momentum is still negative. On the positive side, India’s monetary policy has been increasingly accommodating with interest rates now below the one-year average and high real rates still offering room to manoeuvre. Indonesia is offering attractive valuations versus its long-term average but negative price momentum and weakening growth forecasts for 2020 and 2021 point to a value trap. Meanwhile, in Thailand, negative price momentum and still expensive valuations are outweighing a recent drop in interest rates and an improvement in growth forecasts for 2021.

Scorecard:

Ranked from most attractive to least attractive.

Disclaimer:

For professional investors only. This document is strictly private and confidential and is issued by Milltrust International LLP, incorporated in the United Kingdom, which is authorised and regulated by the Financial Conduct Authority. Milltrust International LLP has its registered office at 5 Market Yard Mews, 194-204 Bermondsey Street, London, SE1 3TQ, United Kingdom and is a subsidiary of Milltrust International Group (Singapore) Pte Ltd.). None of the investment products mentioned herein are regulated collective investment schemes for the purposes of the UK Financial Services and Markets Act 2000. The promotion of such products and the distribution of this document are, accordingly, restricted by law. Most of the protections provided by the UK regulatory system and compensation under the UK’s Financial Services Compensation Scheme will not be available. The investments described herein are only available to investors permitted to invest in the prospectus of the fund and are not available to private investors. The nature of the fund investments carries certain risks and the Fund may utilise investment techniques which may carry additional risk. The value of investments and the income from them may fall as well as rise and is not guaranteed. Past performance is not a reliable indicator of future performance. This document contains forward-looking statements which are correct as at the date of this document. Such statements involve known and unknown risks, uncertainties and other important factors that could cause actual results, performance or projections to be materially different from future results. Any investment in the funds mentioned above should be based on the full details contained in the relevant prospectus and supplements which are available from www.milltrust.com. Notice to US investors: the shares of Milltrust International Managed Investments ICAV and Milltrust International Investments SPC have not been registered under the 1933 Securities Act or under the 1940 Act; however the company takes advantage of the 3[C]7 exemption and shares are available to 3[C](1) US qualified purchasers and those qualifying under Reg D distribution activity in the US is undertaken by Silverleaf Partners LLC, a registered broker-dealer based in New York. Note: Icons used in this document have been created copyright free by authors from www.flaticon.com.