Milltrust International Group is co-headquartered in the asset management hubs of London and Singapore, with a local presence, affiliates, and strategic partnerships spanning across the globe.

Milltrust delivers sustainable investment solutions in public and private markets, focusing on ‘One Health’ and addressing emerging economies, food demand, technology, and climate change, aligning wealth with sustainable prosperity.

Multi-Family Office

East West Private Wealth stands as a premier global Multi-Family office, offering unparalleled, tailored wealth management services and sustainable, eco-conscious investment solutions, crafting legacies across the globe with transparency, flexibility, and integrity.

All the latest news, articles, commentaries, press releases, and media coverage of Milltrust International Group and its affiliates.

Contact Us

Milltrust International Group is co-headquartered in the asset management hubs of London and Singapore, with regional presence and strategic partnerships around the world.

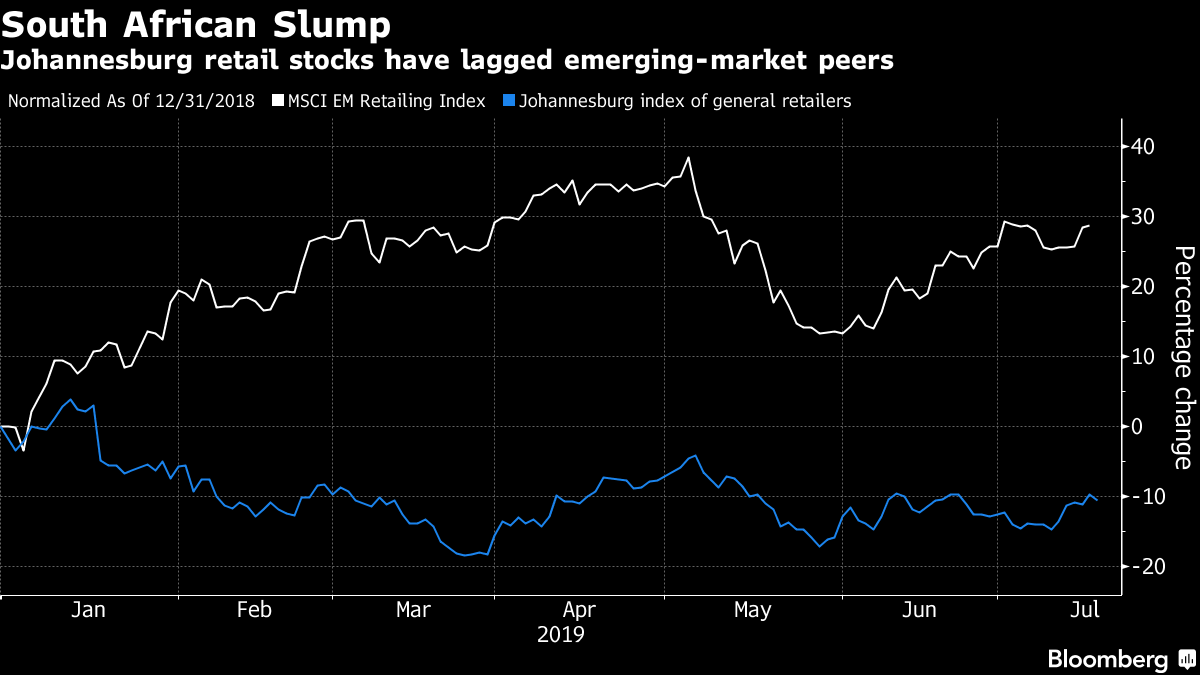

It’s been a tough year for South African retail stocks, battered by gloomy economic news. But hope is on the way.

The South African Reserve Bank is expected to reduce its key interest rate Thursday for the first time since March 2018, starting a series of cuts that economists forecast could total as much as 75 basis points over six months. That would support a fragile recovery in sales and consumer confidence by loosening the cost of debt.

Retail stocks reflect the strain on South African shoppers: an index of general retailers has dropped 10% this year, compared with gains of almost 30% for their emerging-market peers. Durban-based Mr Price Group Ltd. and Cape Town-based Truworths International Ltd. were both among the five worst-performing shares in the developing countries gauge as of July 17.

“Retailers have been among the hardest hit by the consumer being under financial pressure, so any reprieve, even small, will help,” said Nolwandle Mthombeni, an analyst at Mergence Investment Managers in Cape Town. Households spent 9.3% of their disposable income on interest payments on debt in the first quarter and a lower key rate would increase their spending power.

The general retailers index gained 0.2% in Johannesburg as of 12:39 p.m. Thursday. Food and drug retailers were 0.7% higher.

The implications are less positive for South African banking stocks, which have retreated 7% from their 2019 peak in June as expectations build for rate cuts. That’s even offset some of the positive effects of a strengthening rand, which is typically reflected in shares of both lenders and retailers. The correlation between the two sectors has dropped to 0.56 from 0.7 in June, with a reading of 1 indicating the sub-indexes are moving in lockstep.

Bank of America Merrill Lynch strategists, who said July 15 they foresee 75 basis points of cuts within the next six months, estimate the reductions could lift total returns by as much as 20% for retailers. They also see bank stock returns climbing 15% as the rand benefits disproportionately from a risk-on environment in emerging markets.

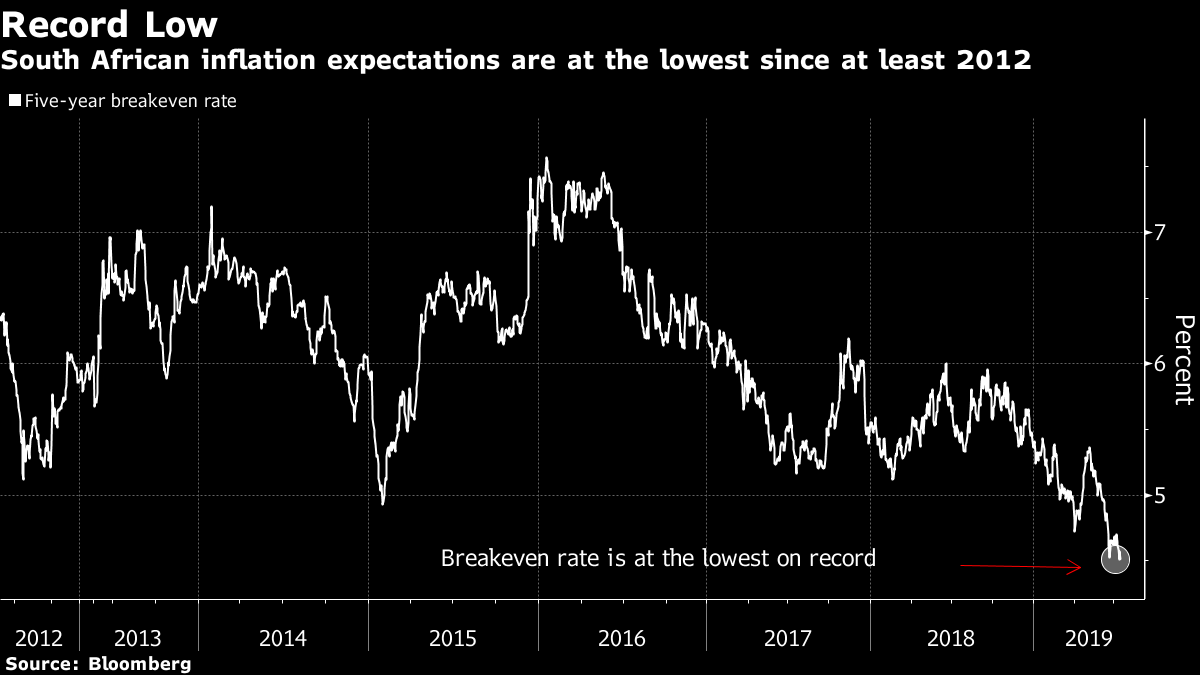

Inflation expectations support policy easing by the South African central bank.

Casparus Treurnicht, a money manager at Gryphon Asset Management, is less optimistic.

“The SARB cutting rates would have a negative effect on bank earnings,” said Treurnicht. “Also bear in mind that the SARB usually cuts rates when economic growth slows down, which might also mean that the net interest margin decreases, and provisions must be made for higher insolvencies.