As we turned into the year’s second half, the markets finally saw more consistent news of better-behaved inflation. With inflation falling closer to central bank targets, some started to signal that they were at or much closer to the point of cutting interest rates. By the end of July and adding in the first day of August, the Bank of Japan, ECB, and UK MPC had cut rates, and the Fed signalled that it would likely cut rates at their September meeting.

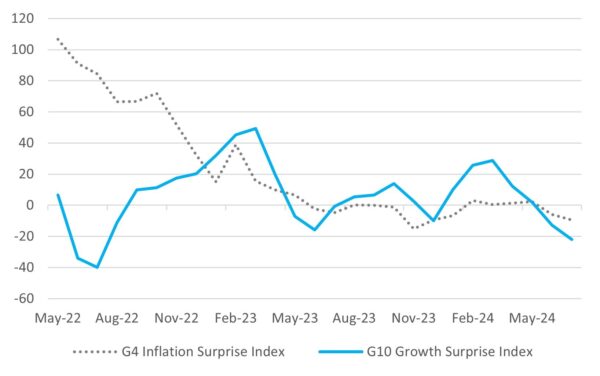

The global growth and inflation surprise indices have moved negatively in recent months. The US appears to have hit a phase of much slower growth, although coming off the back of a second-quarter GDP growth rate of 2.8%, although that growth may have been inflated by a build-up in inventories that may unwind in subsequent quarters.

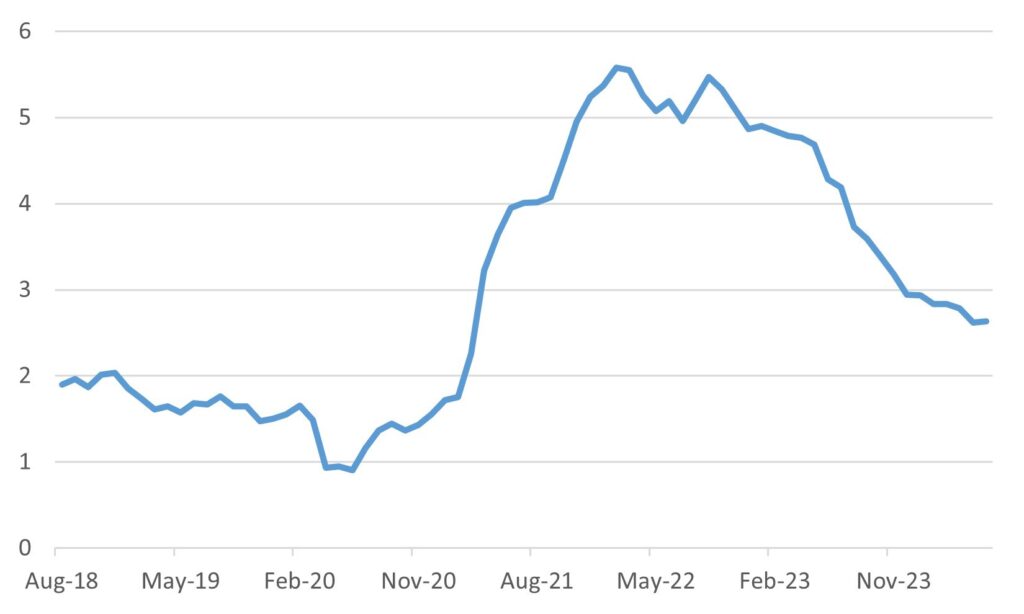

The slowdown in the US economy was most apparent in the labour market, where new jobs rose only 206,000 in July, and the unemployment rate picked up to 4.1%. The Fed has noted the more rapid pace at which the economy is moving to its targets for the looseness of the labour market and the moderation of inflation.

A key feaure of July was the Yen’s sharp reversal of its marked weakness of the previous three months. The Ministry of Finance intervened repeatedly to firstly arrest the Yen’s weakness and then to push it higher against the dollar. At th end of the month central bank tightening of monetary policy will also help the Yen. The BoJ raised its short-term interest rate target to 0.25% from 0-0.1% previously, and said it would taper its bond buying to three trillion yen ($19.53 billion) per month as of the first quarter of 2026.

In the emerging markets, there was a sharp contrast between the good news coming out of India, the disappointing economic data flow from China, and its seeming policy paralysis. India’s budget was a good reflection of still ambitious investment spending on infrastructure and some modestly populist spending in support of the less fortunate. The finance minister also reported a further reduction in the country’s budget deficit and a strong feeling that the government will be able to run a current account surplus in the coming year.

By contrast, China’s economy looks benign, and the crucial Third Plenum meeting of the Communist Party failed to ignite any hope of a near-term boost to the economy. While the government provided a laudable plan for long-term planning, the economy and markets need a transparent boost. As the month closed out, President Xi Jinping acknowledged that the “focus of economic policies should shift more towards benefiting the people and promoting consumption”.